Buoyant markets await latest ECB rate decision

Headlines

*Stocks resume rally with slower rate hike bets

*Meta falls short as revenue decline accelerates

*ECB set to hike interest rates by 75bps, likely to trim bank subsidies

*Dollar slips as chances mount for less hawkish fed, Euro above parity

FX: USD extended its slide against its peers, falling by 1.1% to 109.70. Support on the DXY is the mid-July top at 109.29. The 50-day SMA acts as initial resistance at 110.81. The 10-year US Treasury yield dropped below 4% as risk appetite was curtailed by the tech selloff. The widely watched yield peaked at 4.33% last Friday.

GBP/USD continued higher, up 1.3% and has hit 1.1654 this morning. UK PM Sunak is reconsidering tax rises as an improving economic picture means some of the sweeping measures may be watered down. EUR/USD climbed back above $1 for the first time in a month. USD/JPY closed lower at 146.37 and has sunk again today near to 145.

AUD/USD ended higher and was trading above 0.65 in the Asian session. It closed up 1.7% yesterday. USD/CAD eventually closed lower after printing at 1.3507, even though the BoC only hiked by 50bps. Gold traded to a high of $1675 but is currently capped by the 21-day SMA at $1668.

Stocks: US equities ended a mixed bag with the Nasdaq closing down by 2.26%. Disappointing earnings reports by Microsoft and Alphabet raised concerns about the broader outlook and sent tech stocks tumbling. Both companies suffered their worst one-day declines since the pandemic crisis in March 2020. The S&P 500 was dragged lower and finished down 0.74% but the Dow closed up 0.01%.

Asian stocks traded mixed following a similar lead from Wall Street.The Hang Seng outperformed with tech surging following recent selling. The Nikkei was in the red as exporters were pressured by recent firming in the yen versus the dollar. The ASX 200 was supported by gains across commodity-related sectors.

S&P 500 futures saw two-way action as Meta reported after the bell as rose 8% following a revenue beat. But then Facebook’s owner fell as much as 20% as the group flagged near-term challenges to revenue. European equity futures are modestly lower after the cash markets closed +0.6%.

Day ahead – Pivot trade continues

The BoC “did an RBA” and disappointed market expectations with a smaller 50bp rate hike. The bank clearly stated that further rate hikes will be needed. But policymakers are in the tricky position of fighting persistent inflation with higher rates against overtightening as leading indicators show growth momentum slowing. This conundrum is key for other central banks too.

The rate decision pleased risk markets which are banking on a central bank pivot. The USD is on for one of its worst weeks ahead of US GDP and core PCE data though that is expected to be relatively strong. We note that a slower pace of rate hikes still means financial conditions tighten. It also doesn’t indicate that central banks are about to cut rates, especially with near-term inflation expectations still elevated.

We get Apple and Amazon earnings after the US closing bell. The recent price hikes announced by Apple should mitigate some of the expected weakness in the outlook. Amazon will face triple pressure points in its e-commerce, advertising, and cloud business. The Bank of Japan meeting overnight is likely to stick with its current dovish policies. Softer Treasury yields have eased the pressure on the yen. 145 is a technical focus in USD/JPY.

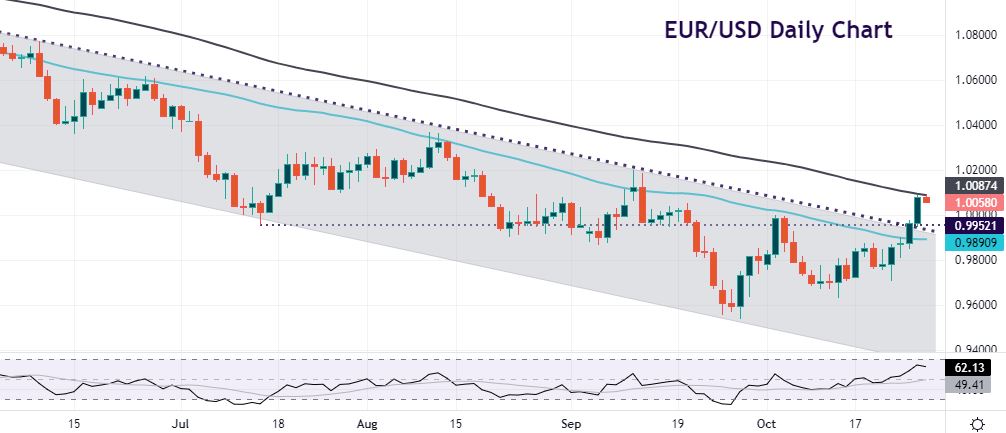

Chart of the Day – EUR/USD hitting the highs

The ECB is fully expected to hike rates by another 75bps which would take the depo rate to 1.5%, its highest since January 2009. We see President Lagarde repeating that hikes of this size are not the norm. Money markets are split between a 50bp and 75bp rate rise in December. The peak rate is forecast at 2.75% next year. The ECB will also have to grapple with stopping banks profiting from rising rates. The issue of quantitative tightening will be a focal point and the unique problem of fragmentation. This is the uneven transmission of policy due to multiple sovereign bond markets across the region.

The ECB has surprised hawkishly all year, but EUR/USD has generally closed ECB days lower. The world’s most popular pair traded higher for five sessions in a row yesterday. That has not been seen since early February. The major appears to have broken out of the long-term bear channel. Near-term resistance is the 100-day SMA at 1.0087. September highs at 1.0187/97 are an upside target. Support sits around the 0.9952 area.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.