Risk mood improves while dollar takes a breather

Headlines

* Dollar buoyed by hawkish Fed expectations as debt deal eyed

* Walmart lifts annual sales, profit view on resilient consumer spending

* Japan CPI quickens again, putting pressure on BoJ view

* Yuan’s biggest weekly loss in three months tests PBoC tolerance

FX: USD rose to a fresh seven-week high after more solid US data. The DXY traded to a top at 103.62 before closing just below. The 2-year yield moved higher for a fifth day. It is now touching its 100-day SMA at 4.24%. The previous pivot top from April is 4.28%. The 10-year yield surged through its 100- and 200-day SMAs around 3.60%. It closed up for fifth straight day just above the April peak at 3.63%.

EUR cracked the 1.08 level and the 100-day SMA at 1.0806. The world’s most traded currency pair closed near its low at 1.0769. Next support is 1.0716. The ECB’s De Guindos said there is stills cope to keep raising rates. But most of the tightening has already been done. GBP broke through the January top at 1.2447. Cable is trading on its 50-day SMA at 1.2408. It hasn’t closed below this since mid-March. USD/JPY burst through the March high and previous resistance at 137.91. The pair has pulled back after making a near six-month high at 138.74. AUD closed at a three-week low at 0.6621. USD/CNH is up ten days in eleven and made a fresh high today at 7.0748. It is severely overbought. Support is the December high at 7.0155.

Stocks: US equities rose sharply for a second straight day. The benchmark S&P 500 finished 0.94% higher and closed at a nine-month high at 4198 right in the resistance zone. The Dow added 0.34% and lagged the Nasdaq 100 which surged 1.81%. It settled at 13834.62, near its high and a close not seen since March last year. Sentiment was supported by encouraging data. This included a surge in the Philly Fed manufacturing survey and a fall in initial jobless claims.

Asian stocks were mostly higher after strong gains Stateside. The Nikkei 225 jumped on the open to its highest since August 1990. But it lost some steam near 31,000. Markets digested the faster pace of acceleration in the latest inflation data. The Hang Seng was pressured as tech suffered after Alibaba’s earnings beat on the bottom line but missed on revenue. Geopolitical tensions reared their head again as the US agreed a “21st Century” trade pact with Taiwan.

US equity futures are very modestly in the green. European equity futures are pointing to a higher open (+0.4%). The Euro Stoxx 50 closed up +1.0% yesterday.

Gold is set for its worst week since January. The stronger dollar and rising bond yields are the key drivers.

Market Thoughts – Fed speakers cast doubt on June pause

We’ve had a phalanx of FOMC officials on the wires all week. Some seem to be sitting on the fence wanting to see the effects of the most aggressive policy tightening cycle in over 40 years. But several have poured doubt on a pause in rates by the Fed at its June meeting. The chances of a 25bps Fed rate hike have increased to 37% this morning. This has more than doubled since a week ago.

Treasury yields have moved higher and are hitting crucial levels and resistance. Of course, this has lifted the dollar even as risk sentiment has improved on debt ceiling deal talk. There is little data out today, but Fed Chair Powell speaks later. Will he shed some light on the Fed outlook for its next meeting? Recent economic releases have been reassuringly solid. Data to justify rate cuts still priced in later this year has eluded markets, so far.

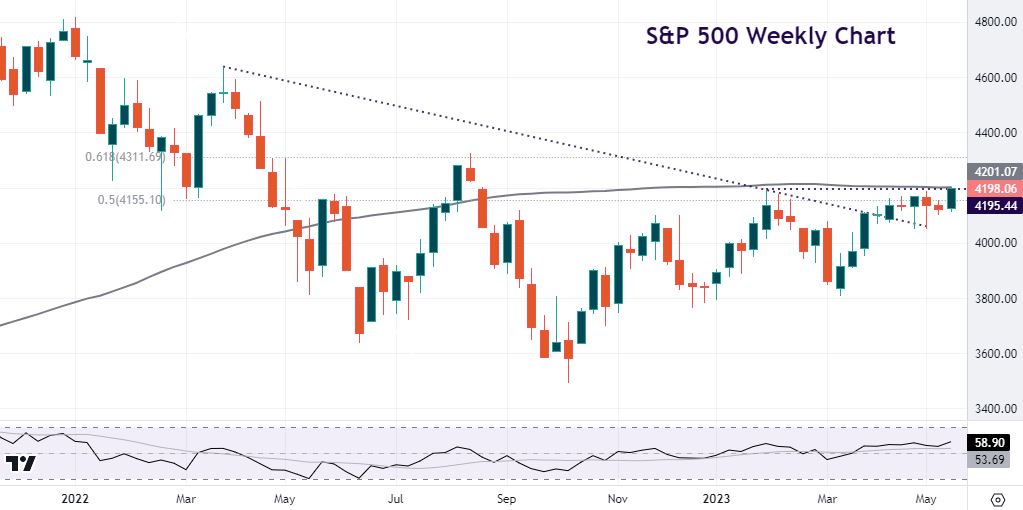

Chart of the Day – S&P500 hits resistance zone

The rally in US stocks is baffling many. The blue-chip index is up 9.3% this year. The tech-heavy Nasdaq has added over 20% in 2023. Q1 earnings have been better than expected, but little was expected of them. There has been a tone of guarded optimism though earnings are down from a year ago. Meanwhile, rising Treasury yields don’t help. The 10-year UST is at its highest level since the SVB failure in early March. Perhaps it’s all the talk about AI which is bringing hopes of a new era in generative computing. Nvidia, the chipmaker who stands to benefit hugely is up 112% this year and is nearing its all-time highs.

The wider benchmark closed just above the key February high at 4195. The 100-week SMA at 4201 plus the psychological mark of 4200 reinforces this area. It goes without saying that the weekly close is crucial for more upside. The next Fib level (61.8%) is at 4311 with the halfway point of the 2022 decline at 4155.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.