Markets remain downbeat with focus on Friday’s US jobs report

Overnight Headlines

*US stocks rose on Friday, but futures are pointing down

*USD retreated amid a decline in US Treasury yields

*Evergrande fallout pushes Asian markets into the red

US equities pushed up on Friday after suffering negative returns in September. The avoidance of a federal government shutdown helped lift sentiment. The S&P500 tumbled 4.8% last month, breaking a seven-month winning streak. The Dow and Nasdaq fell 4.3% and 5.3% enduring their worst monthly returns of the year. Asian markets are showing broad declines today fuelled by the suspension of Evergrande shares. China is closed for a holiday.

USD fell after printing a new high on Thursday at 94.50 and its highest close since September 2020. Amid a drop in Treasury bond yields, the first day of the quarter saw rebalancing flows and real money allocation. EUR gained after five straight losing sessions and is toying with previous support at 1.1604. GBP moved up for a second day and above 1.35. Resistance sits at 1.3571. USD/JPY gained last week, its second straight weekly increase. But the pair is lower for a third day today with support at 110.80.

Market Thoughts – Friday US NFP the main event

It’s a quiet start for the week on the data front as markets continue to be driven by the “stagflation” theme. Evergrande is also grabbing more headlines with trading halted in their shares on the Hong Kong exchange. The company is reported to be selling a 51% stake in its property management unit. This could help ease the liquidity situation which has missed several debt payments over the past few weeks.

High energy prices are putting the heat on central bankers and how they respond to elevated inflation as growth looks to have peaked. Friday’s NFP is obviously key to how and when the Fed acts. A headline 450k should be enough to see an announcement about starting tapering in November. This would consolidate the dollar gains with anything stronger propelling the USD to new highs.

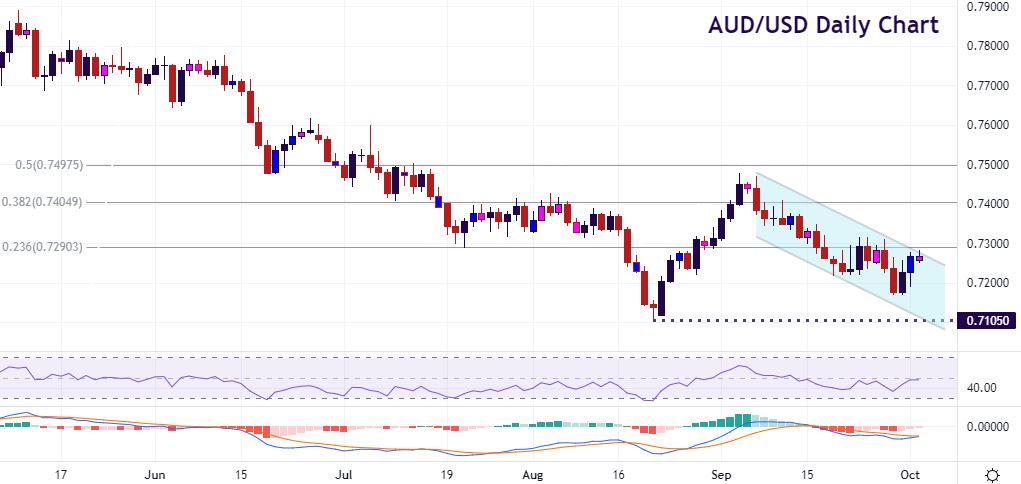

Chart of the Day – RBA meeting non-event

Policy measures are set to remain unchanged at the RBA meeting Tuesday morning. The Board confirmed the reduction in QE to $4bn a week at its previous meeting in September and will keep policy tools frozen until February 2022. Governor Lowe recently confirmed the bank will not increase the cash rate until inflation is sustainably within the 2-3% target range.

The downbeat global risk mood has hurt AUD recently. The risks of financial turmoil in China plus the economic slowdown mean markets are pricing in just 12bp of tightening by the RBA in the next year, much less than its peers. That said, the August low was untouched at 0.7105, after the aussie dipped to 0.7169 last week. Resistance above is the 23.6% Fib level at 0.7290 which is reinforced by the July low.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.