Hot US data tanks tech and boosts the buck

* Stocks fall, US yields rise after strong US economic data

* Dollar gains on reduced Fed rate cut expectations

* Trump threatens economic, not military force, to annex Canada

* Highest UK debt costs since 1988 risk more Labour tax hikes

FX: USD initially dipped below 108 again but buyers stepped in. Hot ISM Services, which expanded for the sixth straight month, and job vacancy data then lifted the buck later in the US session after their releases. Trump also resumed his tariff threats on Canada and Mexico which may have helped dollar bulls. Markets price in just 39bps of rate cut for this year. The recent cycle high sits at 109.53.

EUR underperformed as the single currency failed to benefit from expected, stubborn core inflation data. It matched November’s 2.7% while services inflation remained elevated at 4.0%. Headline inflation ticked higher with the yearly reading moving from 2.2% to 2.4%. The acceleration was driven by energy base effects and has been anticipated by the ECB for some time now. That means it shouldn’t derail easing intentions later this month.

GBP initially picked up to a high of 1.2575 on higher gilt yields before succumbing to dollar strength after the data releases. Those relatively firm UK yields, with the 30-year hitting the highest since 1998, should underpin some support for the pound. That said, cable is in a downtrend from the late September highs above 1.34. The recent cycle low resides at 1.2351.

USD/JPY threatened to break to the upside with a high at 158.42. This is getting closer to previous intervention levels from 158 to 160. The major has a strong correlation to the US 10-year Treasury yield. That looks to be breaking to the upside with yields closing in on last year’s top at 4.73%.

AUD again touched the 21-day SMA, now at 0.6281, before sinking. The recent low is at 0.6178. CPI data is the next risk event for the aussie. Soft data will ramp up RBA rate cut bets and could see new lows. USD/CAD was relatively calm amid the headline havoc around tariffs and the political chaos. Trump threatened economic force to annex Canada. Meanwhile, a domestic election looks inevitable as opposition parties will not support the new government. That is unlikely to happen before May or June.

US stocks: The S&P500 closed down 1.11% at 5,909. The tech-dominated Nasdaq settled 1.79% lower at 21,173. The Dow finished at 42,528, down 0.42%. Tech led the way again, but to the downside this time, with consumer discretionary not far behind. That was essentially down to broad based weakness in the Mag7 names which are again driving markets due to its very narrow breadth. Notably, Tesla lost over 4% and Nvidia was down over 6.2%. The latter had made fresh record highs to kick off the week at $153.13. It unveiled AI-enabled tech to train robot and self-driving cars, gaming chips and its first desktop computer. The chip giant also said it will have “a little bit more” Blackwell chip revenue.

Asian stocks: Futures are lower. Asian markets were mostly higher following on from tech strength on Monday, led by chip stocks and Nvidia. The Nikkei 225, boosted by yen weakness, broke above the 40,000 level. The ASX 200 saw softness in utilities and miners offset strength in tech and telecoms. China was pressured again with heavy losses in Hong Kong. The US Pentagon added names including Tencent to firms alleged to help Beijing’s military.

Gold gained before the US open, up to a high of $2664. But sellers stepped in after the dollar and yields went higher. The 100-day SMA is at $2628 and has offered support to prices recently.

Day Ahead – Australia CPI, FOMC Minutes

The monthly Australia inflation reading is forecast to tick two-tenths higher to 2.3% in November. This is likely to be due to rising housing and food prices. That sais, the RBA recently said it was “gaining more confidence that inflation is moving sustainably to its target”. The statement also suggested “some upside risks to inflation appear to have eased”.

The FOMC minutes are from the hawkish December meeting where the Fed cut rates as expected. But it was a close call with not alot of buy in – four officials preferred no change which is the most dissent in a decade since the dots started. The median dot plot for 2025 predicted just two 25bp rate cuts. Are there more concerns about upside inflation risks than Fed Chiar Powell let on? The minutes will be scrutinised to see how strong the pushback was against more rate cuts and what the threshold for future rate cuts is. Any assumptions around the dot plot will also be a focus, in order to get a sense of the Fed’s reaction function.

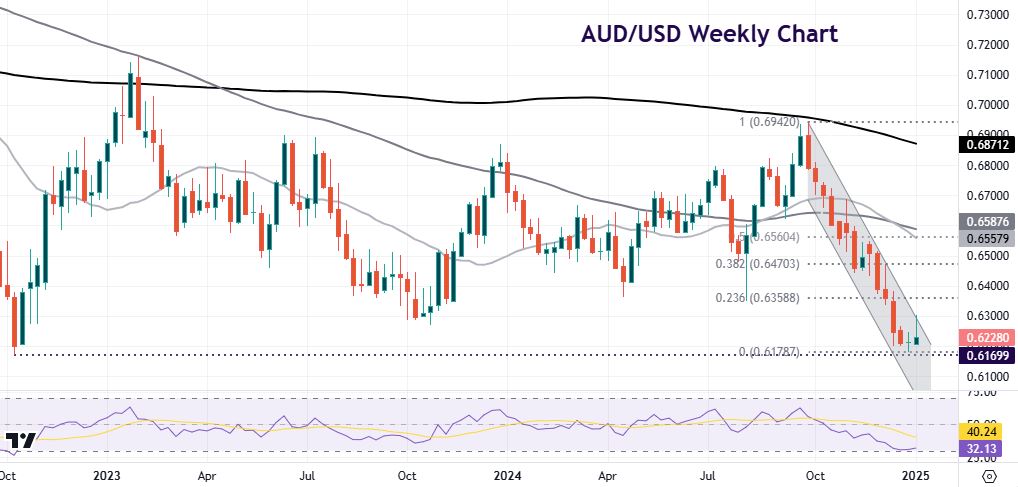

Chart of the Day – AUD close to major support

The aussie was in the bottom three of major currencies versus the dollar last year. Indeed, Bloomberg reported yesterday that leveraged funds boosted their bearish aussie wagers to the most since 2022. Investors are positioning for the upcoming uncertain US policy-making and interest rate path ahead of President Trump’s inauguration with China in the firing line for hefty tariffs. In addition, the RBA is reckoned to soon kick off its policy easing cycle while the Fed is on a protracted pause, according to money markets.

Since topping out at 0.6942 in late September, AUD/USD has fallen in a relatively neat bearish channel. That means a series of lower lows and lower highs. In fact, we’ve had only one down week since that peak. The major is now looking at the low from October 2022 at 0.6169. Lose this on soft CPI and prices could fall below 0.60 relatively quickly. But this is major long-term support.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.