Cautious relief rally sees markets steady

Headlines

* US inflation slows to 6% while Fed weighs its next move

* US dollar finds footing as banking crisis fears calm down

* UK Spring budget to showcase improved financial landscape

* China’s economy shows mixed recovery from Covid slump

FX: USD closed largely unchanged at 103.59. The DXY is being supported by its 50-day SMA at 103.43. After popping up above 30, the Vix has fallen back to 23. The US Treasury 2-year yield rebounded strongly after posting its biggest three-day slump since 1987. It saw its largest daily rise since June last year. Markets focused on the hot US inflation data. The 10-year yield also closed higher. This resulted in the spread between the 2s and 10s inverting again.

EUR closed near its recent highs at 1.0733. The major has made a fresh top at 1.0759 this morning. GBP was a touch weaker ahead of the Spring budget statement announcement today. Cable settled at 1.2158. Mixed jobs and wages data was released on Tuesday. USD/JPY ended the day higher at 134.22. It bounced off its 50-day SMA at 132.54 on Monday. AUD closed 1.1% higher and is trading around the July 2022 low. USD/CHF has found support near recent lows Safe haven buying pushed the major close to fresh year-to-date lows at 0.9059.

Stocks: US equities had a positive session as regional banks led the gains. The benchmark S&P 500 closed up 1.6% after a volatile day. It still remains below the 200-day SMA at 3939. The tech-laden Nasdaq 100 closed higher by 2.32%. META shares jumped 7% after the tech giant announced a further 10k job cuts. The Dow added 1.06%. The KBW bank index snapped a six-day losing streak to close up 3.2%. But it does remain far below its highs for the year. According to analysts, it hit a more oversold level on Monday than it ever touched in 2008.

Asian stocks were mostly positive following wall Street’s lead. Investors digested mixed Chinese activity data. The Nikkei 225 was choppy heading into the conclusion of the spring wage negotiations. The Hang Seng traded higher driven by strength in tech and developers.

US equity futures are modestly in the green. European equity futures are pointing to a slightly firmer open. The Euro Stoxx 50 cash market closed up 2.02%.

Gold gave back some of its recent gains. It has steadied around $1900 after the mostly inline Us inflation data and sharp rebound in US Treasury yields.

Day Ahead – More US data as markets steady

The latest macro data and news is not really giving the Fed any excuse to not hike rates at its meeting next week. The US banking sector found some solace from the lack of news regarding any more bank failures. The CPI data printed mostly in line with expectations but remained at elevated levels. Recent trends remain intact – energy and core goods prices continue to drop while services and food maintain their upward trend. Shelter is still key, the biggest component and expected to fall in the coming months.

Today’s US retail sales will inform on the health of US consumers, though how much they will be affected by the recent banking blow-up could render this data rather stale. PPI data is expected to show a decline but is still too high. The key question for the Fed is whether to hike rates again to fight sticky inflation or pause to assess the damage from the banking issues. Essentially it is a question of keeping separate its efforts to keep banks liquid from hiking interest rates. Money markets see a strong chance of the latter still (80%). That means they essentially only give a 20% likelihood of more bank pain.

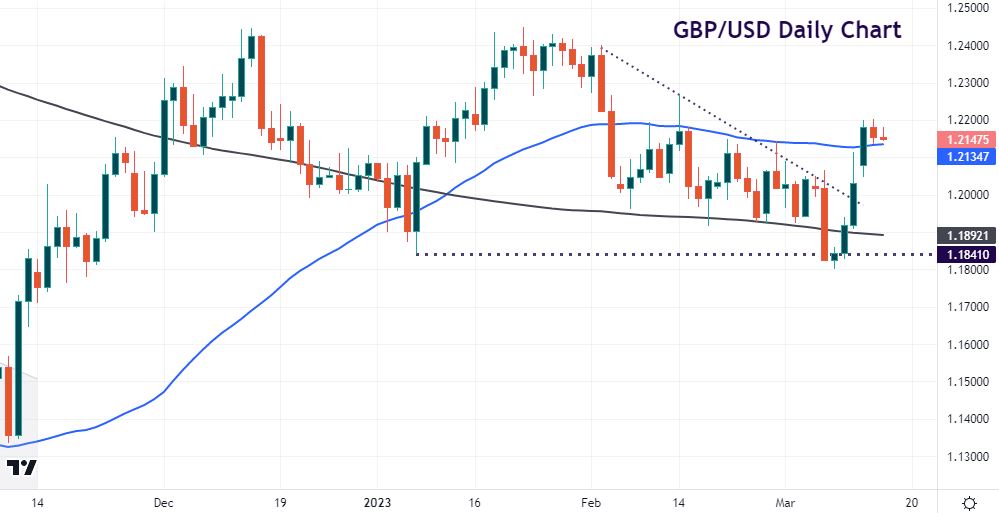

Chart of the Day – GBPUSD holding onto support

We had some important UK data out yesterday in the form of earnings and job numbers. It seems momentum is fading in wage figures and wage growth expectations among firms appears to have peaked. Taken with the dip in core services inflation, next week’s BoE decision is more uncertain. The bar for pausing rate hikes is much lower than for the Fed and ECB. Today’s budget shouldn’t really move the dial though the fallout from the SVB collapse lingers.

After four strong days of gains, GBP/USD has paused for breathe above its 50-day SMA at 1.2134. A bull flag could be developing if prices hold above this support, with the near-term target at 1.2269. But the loss of that support could see 1.2050 fairly rapidly.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.