Markets await NFP in holiday thinned liquidity

Headlines

* USD steady but near recent lows as US employment data looms

* GBP is the best performing major currency this year amid cautious optimism

* US stock indices end higher helped by Alphabet

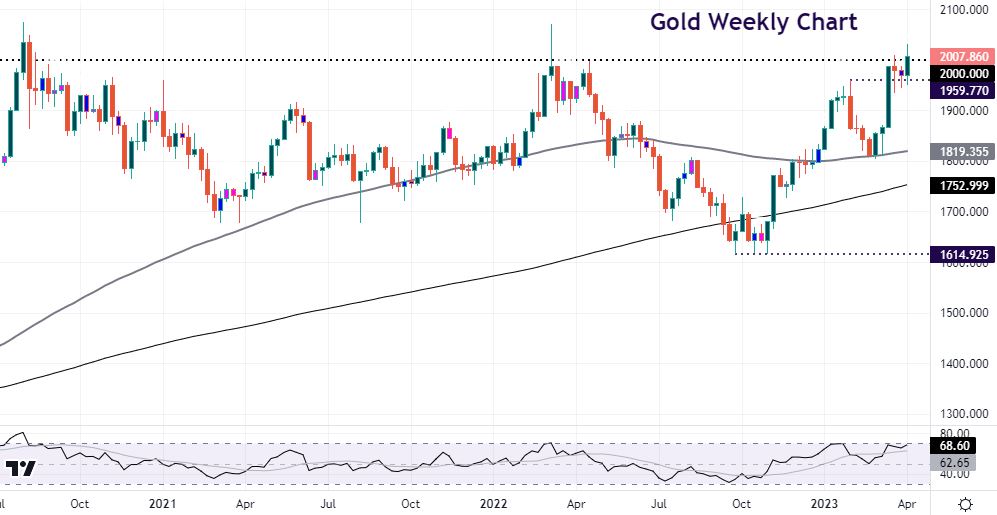

* Gold falls and touches $2000 but remains above key level

FX: USD traded in a narrow range yesterday as bulls struggle to make any headway against the solid medium-term downtrend. This week’s low is at 101.41. The February bottom is at 100.82. The US Treasury 2-year yield bounced, the first green day in five. All eyes are on the NFP data. The 10-year yield closed down for seven straight days in a row making a seven-month low at 3.25%. Prior support at the January low is at 3.32%.

EUR made headway and kept above 1.09. This week’s high and resistance sits at 1.0973. GBP is trading around the previous year-to-date high from January at 1.2447. USD/JPY bounced as yields did too but is still languishing below 132. The AUD remains below 0.67 and the 200-day SMA at 0.6745. NZD plunged 1.19% and traded near 0.6250. USD/CAD rebounded for a fourth day back to a Fib level at 1.35.

Stocks: US equities finished higher as tech bounced. The benchmark S&P 500 added 0.36%. The Nasdaq 100 closed up 0.74%. The Dow edged higher 0.01%. Alphabet shares rallied 3.8% and Microsoft climbed 2.6%. The former’s Google unit plans to add artificial intelligence features to its search engine, according to the WSJ.

Asian stocks were mixed ahead of the holiday period and US jobs data. Most markets were closed for Easter. The Nikkei 225 declined while Shanghai gained with the Hang Seng closed.

Gold dropped to $2000 but is hovering above this level with the focus on today’s labour market data.

Day Ahead – NFP still expected to remain relatively solid

As we said yesterday, most of the economic releases this week have played into the slower growth narrative with ISM data generally disappointing. The JOLTS job vacancy numbers came in much lower than expected with the lowest print since May 2021. Consensus for today’s NFP sees around 235,000 job gains in March. The jobless rate is likely sticking at 3.6% and average hourly earnings are forecast to tick higher to a relatively benign 0.3%. The headline number has continued to surprise to the upside over recent months with 311k new jobs created in February and only marginal revisions. But yesterday’s jump in initial jobless claims hit the so-called “whisper number”.

The odds have flipped back and forth as to whether the FOMC hikes rates by 25bps or stand pat at its meeting at the start of next month. It is currently pretty much a coin flip as to what they do. The dollar could be on track for four straight weeks of losses. That hasn’t been seen since August 2020. But the week’s soft data does seem to be baked into expectations now. Anything above 200k would still be seen as solid job gains. This should flip the odds towards a 25bp May hike and support the struggling dollar.

Chart of the Day – Gold remains above $2000

Gold has closed above the crucial psychological $2,000 this week for the first time since March 2022. Recent US data has crumbled with the job market loosening and fuelling expectations that the Fed is nearing the end of its rate hike cycle. Gold has also benefitted over the last month from increased safe-haven demand given concerns from the banking sector.

Treasury yields have made fresh cycle lows this week and risk sentiment has also wavered. The precious metal printed a fresh high at $2032 and a “doji” candle on Tuesday. This signals some indecision with prices opening and closing at similar levels in the middle of the day’s range. Much depends on NFP, with a soft report cementing a strong close above $2000 and within striking distance of gold’s all-time high of $2,075 hit in August 2020. Support sits at $2k and $1959.

The information has been prepared as of the date published and is subject to change thereafter. The information is provided for educational purposes only and doesn't take into account your personal objectives, financial circumstances, or needs. It does not constitute investment advice. We encourage you to seek independent advice if necessary. The information has not been prepared in accordance with legal requirements designed to promote the independence of investment research. No representation or warranty is given as to the accuracy or completeness of any information contained within. This material may contain historical or past performance figures and should not be relied on. Furthermore estimates, forward-looking statements, and forecasts cannot be guaranteed. The information on this site and the products and services offered are not intended for distribution to any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.